Date: 2015-10-31

Background

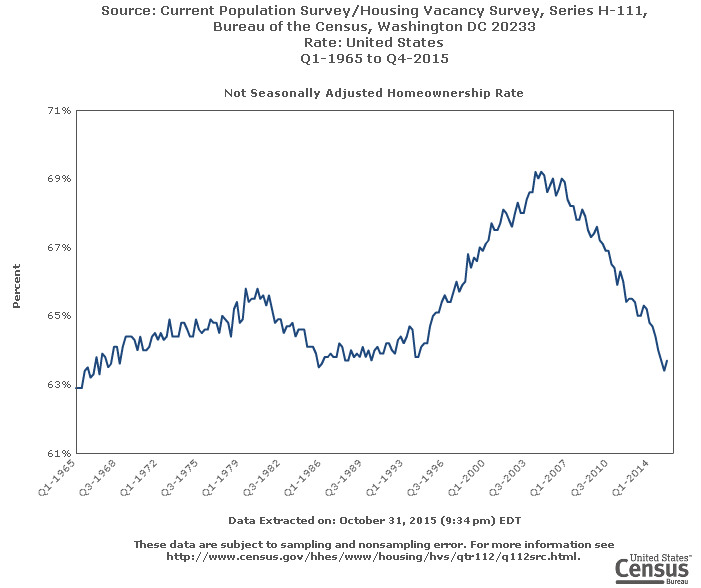

It is common saying that home ownership builds wealth and provides tax shelter. But a lot of homeowners were deep in debt and were forced to sell their homes from 2011 to 2013. The home ownership rate decreased from its high of 69% in 2007 to 63% in 2015 (source: US Census)

This brings the question: does home ownership still build wealth. That’s a question I wanted an answer, especially after I became a real estate agent recently – I want my clients to make the best decision under his/her circumstance.

Did home ownership build wealth before?

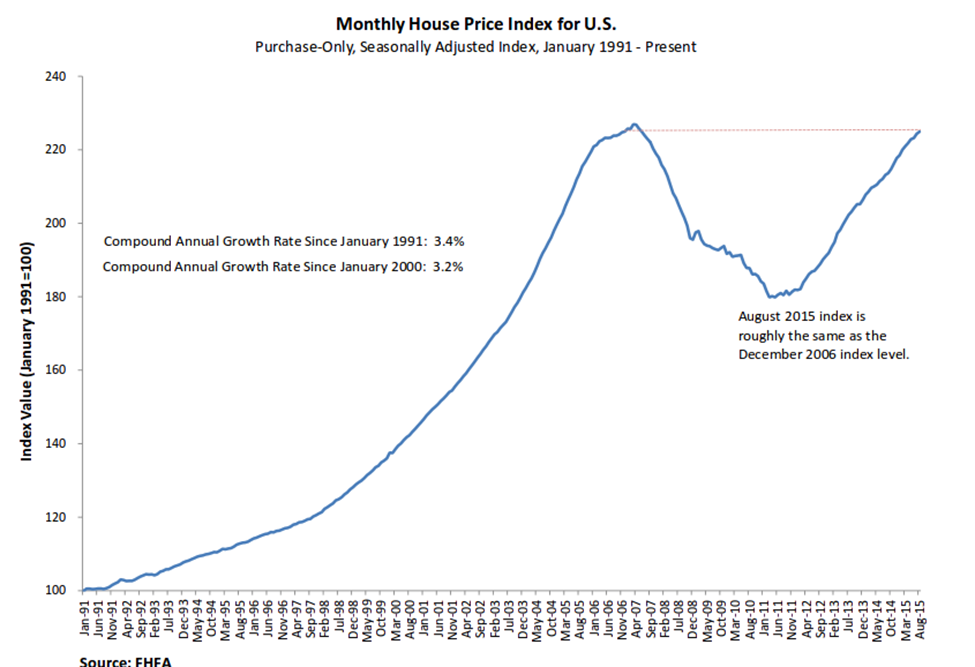

To predict the future, one has to look back to the past. According to Federal Housing Finance Agency (FHFA) monthly House Price Index (HPI), house price increased from 100 to 230 in 2007, then dropped back to 180 in 2011 and recovered to 230 in Aug 2015.

|

Time Period |

Increase | Number 0f Year |

Average Increase/Year |

| 1991 – 2007 | 230 – 100 = 130 | 16 | 8.125% |

| 2007 – 2011 | 180 – 230 = -50 | 4 | -12.5 |

| 2011 – 2015 | 230 – 180 = 50 | 4 | 12.5 |

| 1991 – 2011 | 180 – 100 = 80 | 20 | 4.0% |

| 1991 – 2015 | 230 – 100 = 130 | 24 | 5.416% |

House price fluctuated in short term, but it increased in long term. If one purchased a house at 1991 and sold it at the depth of the housing recession of 2011, the house still appreciated 4.0%/year.

Hold on, was the price increase caused by inflation? That is a valid question. Let’s check the inflation during this period.

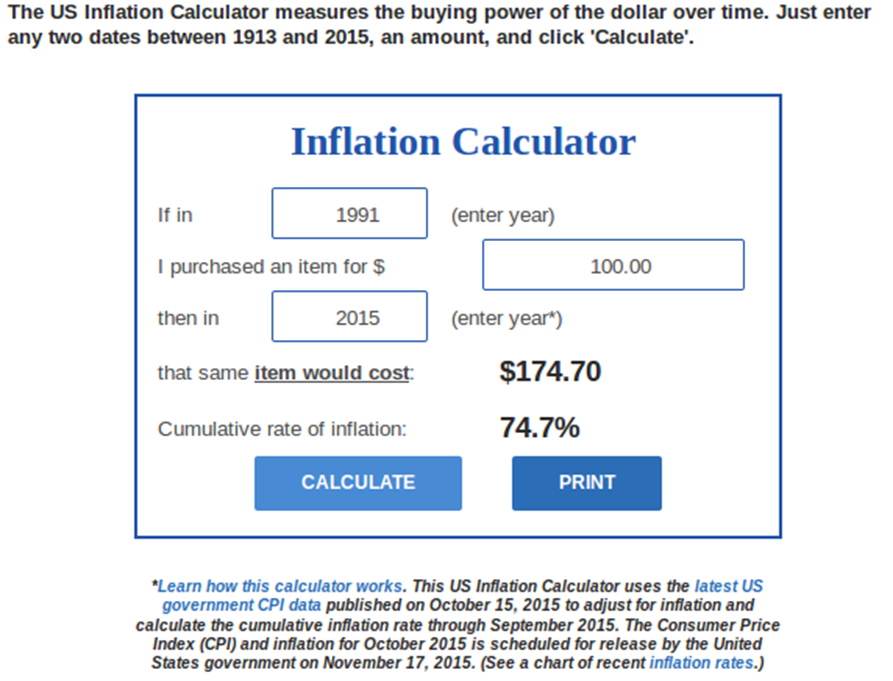

Using an inflation calculator, total inflation from 1991 to 2015 is 74.7%. Average annual inflation was 3.11%.

Even the owner sold the house in 2011, the house price appreciation was higher than inflation by 0.89%. For last 24 years, home price appreciation was 2.30% higher than inflation (5.416% vs 3.11%). The extra 2.3% can add up over a long period – it doubles the original amount in 31 years!

Home ownership did build wealth for long term home owners!

Does home ownership provide tax shelter?

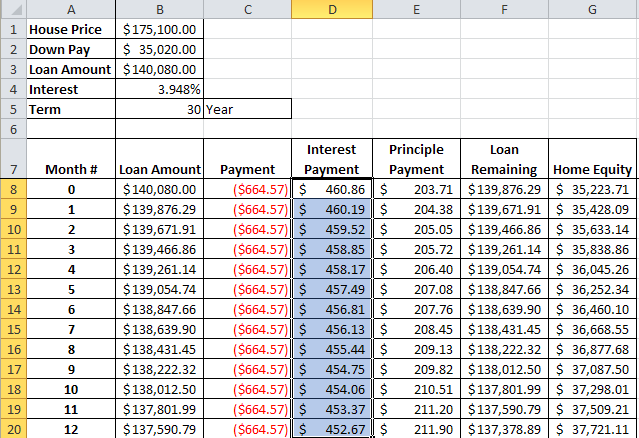

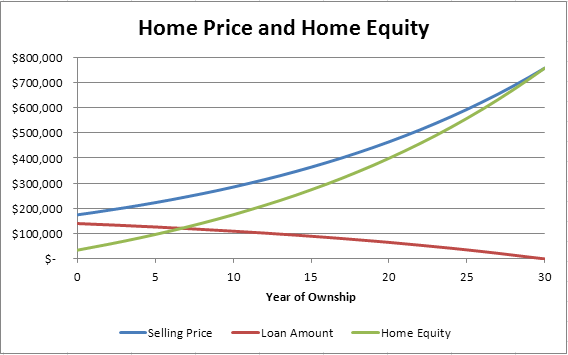

To answer this question, one has to use some real world number. I picked a median price house for Gwinnet, which was $175,000 in 2015. The house was built in 1980 in Suwanee with 1,116 ft2, 3 bed rooms and 2 full bathes.

Internal Revenue Service (IRS) allows tax filers either take standard deduction or itemized deduction. If itemized deduction is used, only interest payment is allowed.

Current interest rate is 3.948% for 30 year mortgage with 20% down payment. An Excel spreadsheet is created to calculate monthly payment, interest payment and principle payment. First year’s payment calculation is shown below:

First year has the highest interest payment (when loan balance decreases, interest payment decreases with it). First year’s total interest payment is $5,938.

IRS’s website showed that standard deduction for single filer was $6,200 and $12,400 for married filed jointly in 2014. The owner of this median priced home probably would not enjoy any annual tax benefit.

Home ownership likely does not provide annual tax saving.

However, IRS also allows capital gain exclusion of up to $250,000 for single filer and $500,000 for married filed jointly. If the house price increases 5% per year in next 30 year, owner of the house above would reach $500,000 capital gain in about 27 years (house price $675,100). That capital gain is tax free if owner meets IRS requirements.

Home ownership does provide capital gain protection.

Conclusions

Home ownership is still a good wealth building tool and it also provides capital gain tax protection.